Altri - small Portuguese company.

Low valuation multiples with above-average growth. Pending approval of its project in Lugo. Skin in the game.

Discover Altri: A Portuguese small cap with €980 million market capitalization. Specializing in forest management, cellulose production, and renewable energy, it offers low valuation multiples and impressive growth potential. With a pending project in Lugo focusing on sustainable textile fibres like Lyocell, Altri presents an enticing opportunity for investors looking to ride the wave of eco-friendly innovation and financial prosperity.

Altri is a Portuguese company that was established in 2005 through the restructuring of Cofina and various acquisitions in the early years, including notable ones like Celtejo, EDP Biolectrica, and Celbi, which it acquired from Stora Enso. Currently, it has a market capitalisation of €980 million and went public in 2005, experiencing a remarkable 1,670% appreciation since then. It currently trades at a P/E ratio of 3 times, achieves an ROIC exceeding 10%, which is above the market average, and has increased its sales by a 12% CAGR since 2021.

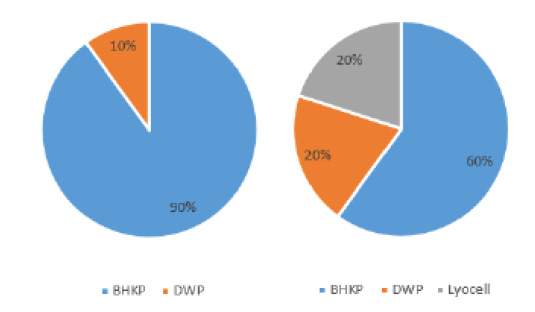

Altri, headquartered in Oporto, is a conglomerate that manages forests and produces and markets cellulose. Additionally, it generates and sells renewable energy from biomass. It operates three plants in Portugal with a capacity of over one million tons per year. Just over 50% of its sales consist of tissue paper, with its primary market being Europe (excluding Portugal) accounting for approximately 60% of its sales. The group also manages around 85,000 hectares of forests.

Altri is outstanding in electricity generation. The energy used in its factories is produced in cogeneration plants, entirely from renewable fuels. Cogeneration is the process by which by-products of cellulose production, derived from wood, are valorised, producing steam and electrical energy. This way, the factories' needs are met, and the surplus is injected into the national electrical grid.

Company and Market Outlook

It is expected that the global demand for pulp will increase by 2.1% annually until 2027. The robust demand in China is driving global demand upward despite the weakness observed in Europe and North America. Pulp prices experienced a significant decline in 2023, reaching a minimum of $809 per ton, causing many companies to suffer and substantially reduce their profit margins. Pulp prices in China are already on the rise, and a similar trend is expected to follow in Europe soon. By 2024, a normalisation is expected, reaching around $940 - $1,000 per ton.

Regarding Altri, they expect to have the Gama project up and running this year, located in Galicia, specifically in Lugo. The project entails the establishment of a plant for the production of sustainable textile fibres known as Lyocell. This project positions Altri as a global leader in the production of this material, which is manufactured in an environmentally sustainable manner.

Altri anticipates that with Gama, the company's revenues will be more diversified. This would provide the company with greater stability and improve its financial balance. In addition to increasing sales, the global market for textile fibres is expected to grow at a rate of 7-8% annually until 2030.

Mentioning that, despite the normalization of pulp prices, the company could maintain its profit margins. This could be achieved by offsetting the decline in energy prices, increasing sales volume, and in the future, with the production and sale of Lyocell through its Gama project.

How is Gama going? Ongoing studies are paving the way for a final investment decision (FID) in the near term for the Gama project, slated for the Palas de Rei area in Lugo, Galicia, Spain. Announced as a potential location in April 2022, the 200-hectare project gained approval as a 'Strategic Interest Project' in December 2022, expediting licensing processes. The upcoming steps include an environmental impact study, a detailed engineering plan, economic viability assessment, the pursuit of EU subsidies, and acquiring necessary licenses from authorities.

Management Team and Shareholders - skin in the game.

José Armindo Farinha Soares de Pina has been the CEO and director of Altri since 2020. Carlos Alberto Sousa Van Zeller e Silva is the deputy CEO and director of operations, who recently joined the company. Vítor Miguel Martins Jorge da Silva, the CFO, has also been appointed as the CEO of the Galician subsidiary that will manage the textile fibre factory, accompanied by Carlos Sousa. All of them have over 10 years of experience, and their salaries do not exceed €3.5 million. These salaries seem somewhat excessive, which is a negative point for the management team.

The top five largest shareholders of Altri collectively own more than 65% of the company. Among them are companies led by members of Altri's board. Promendo is led by Ana Menéres Mendonca, Canderno Azul is managed by Joao Manuel Matos, vice president of Altri. Domingos José Vieira de Matos, one of the founders of Cofina (the company that led to the creation of Altri through a spin-off), has been involved in managing the group since its inception. He is the director and majority shareholder of Livrefluxo, S.A. Paulo Jorge dos Santos is the director and majority shareholder of Actium Capital. Lastly, 1 Thing Investments has Pedro Miguel Matos Borges de Oliveira as an advisor on its board, who also serves as an advisor in Altri.

Some key figures.

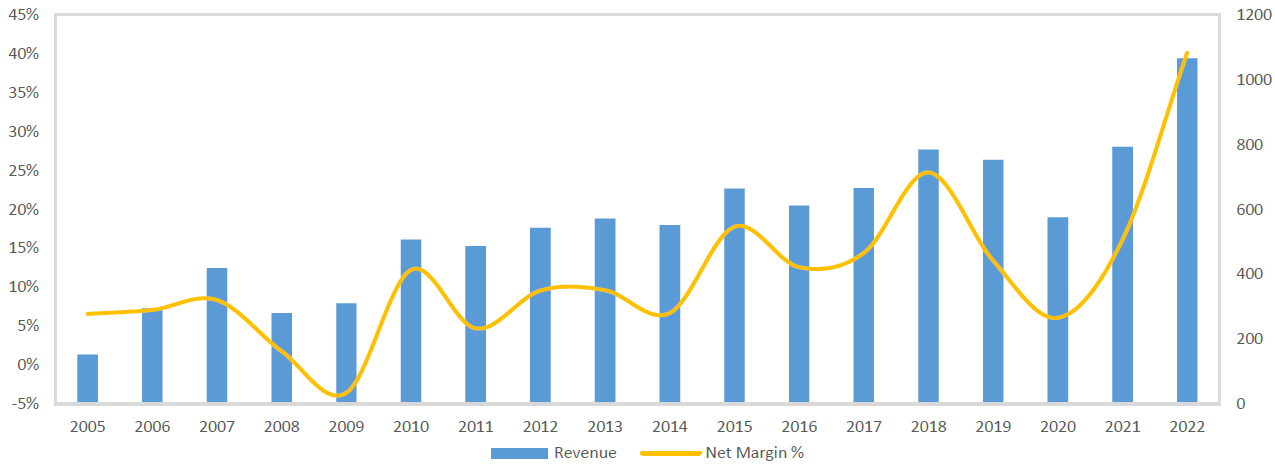

Over the last 10 years, Altri has increased its net profit by 51%, with a CAGR of 35% in the last 5 years. The company has managed to maintain an average operating margin of 16%, while its competitors typically hover around 10%. In 2022, it recorded revenue of €1,066.20 million, a 34.40% increase from 2021. However, it posted a negative free cash flow of -€220 million, the first time in its history, attributed to investments in new projects. Nonetheless, the company maintains a robust balance sheet, with reduced debt currently at €438 million.

In the following graph, we can observe that in 2020, the company faced challenges as pulp prices dropped by 22% compared to the average price recorded in 2019, and it was impacted by the effects of the COVID-19 pandemic.

There are good reasons to believe that Altri's results will continue to improve as pulp prices rise, demand increases as expected, and the Gama project begins to operate. The company's operations report EBITDA margins of over 20%, and I anticipate these margins to expand in the coming years. Additionally, with the decline in energy prices, the company will reduce costs, leading to increased revenues and margins.

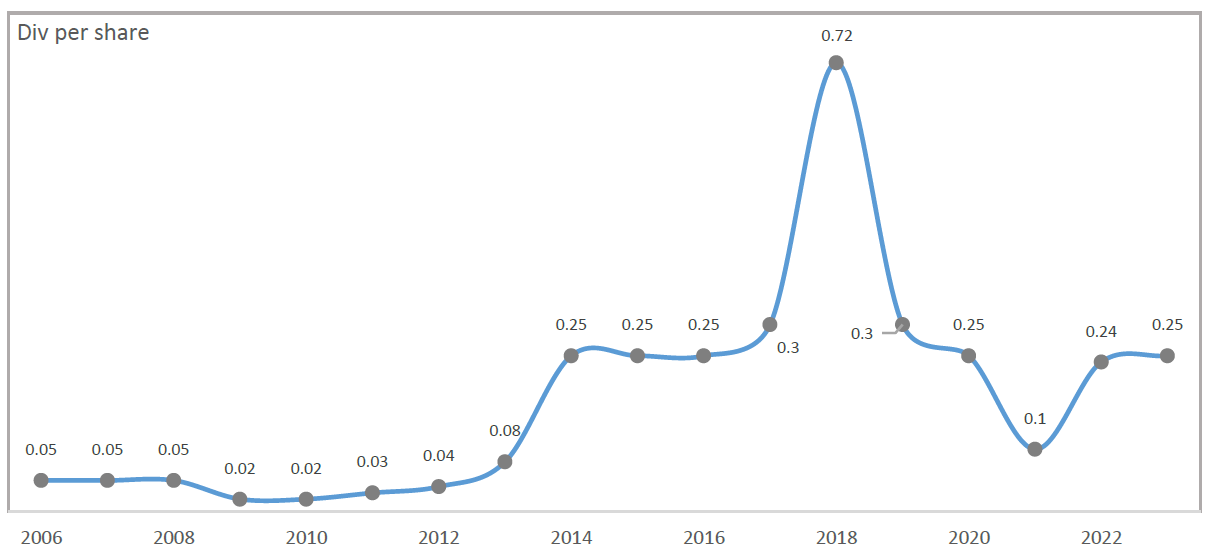

It's worth noting that the company does not have a sustained dividend policy. Their objective is not focused on dividend distribution, as they have room to continue investing in growth.

Despite the growth, positive future outlook, and excellent capital returns, Altri is trading at a P/E ratio of 2.3x, significantly below its historical average of over 7x and the sector average of 10.6x. This suggests that the company may be undervalued. Additionally, the EV/EBITDA ratio is at 5.3x, well below the sector average. Notably, well-known companies in the sector like Navigator or Stora Enso trade at higher multiples.

The returns are impressive, and I expect them to be sustained in the long term. The only company that competes with Altri in terms of returns is Navigator.

However, despite these positive figures, the company is not without risks. The main risks include a decline in cellulose and energy prices, delays in the Galicia project, natural disasters, new regulations, or unexpected shutdowns at any of its three factories in Portugal.

Altri is somewhat illiquid, which is not necessarily a drawback. Illiquidity allows for the acquisition of a company at a lower valuation than in a liquid market. Investors can enable the company to work for them with less volatility, generating value year after year. Typically, shares of a good company become more liquid over time as investors begin to take notice. Altri's illiquidity is attributed to its size, sector, and the country in which it operates. However, I do not doubt that with the rise of ESG, more funds in this category will focus on it and start investing.

Valuation.

For the valuation of Altri, a DCF analysis will be used until 2027 with a discount rate of 9% and a terminal growth rate of 2%. An EBIT margin of 18% for the next 4 years, slightly lower than previously recorded, and finally, a risk-free rate of 3.8% to stress the value. This results in a valuation of €7.25.

If I value using multiples, assigning a P/E ratio of 9x, an EV/EBIT of 8x, and an EV/FCF of 12x, we obtain a very similar target price of €9.38. If we weigh each valuation equally, I have a weighted target price of €8.31, representing an upside of 85.58% from the current prices (€4.48).

The valuation is conducted in a neutral scenario, although I usually incorporate a 5% margin of error on the price in case my projections turn out to be too optimistic and vary. Applying this discount, I obtain a target price for the company of €7.90, representing a 76% increase.

Conclusion.

The company appears interesting, with quite attractive growth potential. However, investors must have a truly long-term perspective, as the company will not reach its true value overnight, due to the factors mentioned earlier. What is clear, though, is that the prospects for the company are positive, with the Gama project in Galicia expected to significantly boost revenues and, above all, provide greater diversification.

Disclaimer: This is a personal analysis and does not constitute any buying or selling recommendations. Each investor should make their own due diligence.

Do not support this company nor industry. So much bs greenwashing. Paper mills do not “manage” forests, they destroy them and replace them tree farms, sad shadows of forests which are harvested again and again and never allowed to heal or mature. Ground water suffers, ecosystems collapse. It’s shameful. The future is in reusable, and small scale local projects which keep environments in tact. Stop this.

Intriguing how a cap intensive cyclical co can compound and valued at such low multiple? What do you think the company is like in 10-20 years?