Brief Summary: Lion Rock Group is a founder-led, vertically integrated global book printing and publishing platform, specialising in illustrated, educational, and speciality titles. Founded by Chuk Kin Lau and listed on the Hong Kong Stock Exchange, the Group has grown through disciplined acquisitions and strategic geographic diversification. With steady revenue and EBITDA growth, a strong net cash position, and a focus on resilient niches, the company currently trades at an EV/EBITDA of 2.0x, P/E of 5.3x, offers a dividend yield of approximately 8%, and a free cash flow yield above 12%.

Company Overview

Lion Rock Group Limited is a Hong Kong–based printing and publishing platform listed on the Main Board of the Hong Kong Stock Exchange. The company has developed into a globally integrated book production platform generating more than €280 million in annual revenue. It originated from 1010 Printing, founded in 2005 and separately listed in 2011 before the group was renamed Lion Rock Group. The name draws inspiration from Hong Kong’s Lion Rock, a symbol of the city’s core values, resilience, hard work, perseverance, and solidarity in the face of adversity.

The Group is led by founder and Chairman Lau Chuk Kin (CK Lau), a self-made entrepreneur with more than three decades of industry experience. Prior to founding Lion Rock, he built a reputation for disciplined capital allocation during his tenure at Recruit Holdings, where shareholders reportedly achieved a compound annual return of approximately 23 % over thirteen years. His emphasis on conservative balance sheet management, disciplined acquisitions and long-term value creation has shaped Lion Rock’s strategic development.

Since 2012 the Group has pursued a selective acquisition strategy to expand its geographic footprint, strengthen vertical integration and increase production capacity. Key transactions include the acquisitions of Asia Pacific Offset in 2012, Opus Group Limited in 2014, Singapore-based COS in 2016, and an investment in the illustrated publisher The Quarto Group beginning in 2017, with Lion Rock increasing its stake to over 49% by April 2022. Additional acquisitions include Papercraft in Malaysia and the UK book printer Clays Ltd in 2020, and Griffin Press in 2022. The Opus Group business was later stabilised and separated through the listing of Left Field Printing Group. These transactions were generally executed at disciplined valuations and materially expanded the Group’s international presence.

Note:Left Field Printing Group currently trades at 7× earnings and 2.10× EV/EBITDA, offering an 8.6% dividend yield and a free cash flow yield of over 28%. Lion Rock Group holds approximately 62%, while Lau indirectly controls additional stakes through ER2 Holdings Limited and Lion Rock, resulting in a combined holding of around 70%.

The company has also undertaken limited treasury investments as part of its capital management strategy, including the purchase of a US$10 million credit-linked note in August 2024. While immaterial relative to operating activities, such investments illustrate management’s opportunistic yet conservative approach to capital deployment.

Today Lion Rock operates a vertically integrated global book production platform spanning several stages of the publishing value chain. Operationally, activities fall into four areas, which are consolidated into two reporting segments: Printing and Publishing.

Print Manufacturing. The Group operates large-scale printing facilities in Mainland China, Malaysia, Singapore, the United Kingdom and Australia. Its flagship 1010 Printing plant in China covers approximately 600,000 square feet. Production focuses on higher-value illustrated formats including cookbooks, art books, children’s titles and educational materials, which are less susceptible to digital substitution. Major clients include Penguin Random House and Simon & Schuster. Around 50% of revenue is generated from the United States and roughly 30% from Australia.

Print Management. Through Asia Pacific Offset and Regent Publishing Services, the Group provides sourcing, procurement, logistics coordination and quality control services for publishers. This intermediary function consolidates production volumes, manages complex printing schedules and supports utilisation across the Group’s manufacturing base.

Creative Publishing. Lion Rock’s majority investment in The Quarto Group provides exposure to the publishing segment, particularly illustrated titles across arts, crafts, gardening, cookbooks and children’s books. The integration enhances margins and provides insight into end-market demand and publishing trends.

Print Consultancy. Through Libermata, the Group offers publishing workflow solutions and procurement optimisation services, leveraging its supplier network to reduce sourcing costs for publishers.

Lion Rock’s vertically integrated structure supports procurement scale, cost management and operational flexibility across jurisdictions. Proprietary ERP systems streamline coordination between customers, suppliers and production facilities, while the Group maintains stringent environmental, social and governance standards.

Although the global printing industry faces gradual structural pressure, Lion Rock’s focus on illustrated and educational formats, segments less exposed to digital substitution, provides relative resilience. The Group has also mitigated geopolitical risk, including potential U.S. tariff exposure on Mainland China production, by expanding manufacturing capacity in Malaysia.

Overall, Lion Rock combines disciplined capital allocation, geographic diversification and vertical integration, positioning the company as a resilient global platform within a specialised niche of the publishing value chain.

Market Commentary

The global book printing market is mature and generally stable, with limited structural growth but relatively predictable demand. While certain categories, such as mass-market fiction, have experienced long-term pressure from digital formats, illustrated and educational books remain resilient. Cookbooks, art and photography books, children’s titles and textbooks continue to favour print due to their visual quality, durability and tactile appeal. These higher-value segments form the core focus of Lion, helping to support margin stability despite broader industry headwinds.

The publishing supply chain is highly international. Major end-markets, including the United States, the United Kingdom and Australia, depend significantly on Asian manufacturing capacity because of cost competitiveness, scale and technical expertise in colour printing and complex binding. However, geopolitical considerations, including US tariffs on certain Mainland China imports, have increased the importance of production diversification. Even though book tariffs remain relatively low, publishers and printers are increasingly prioritising flexibility by expanding capacity in alternative locations such as Malaysia to reduce concentration risk.

Recent years have also highlighted the importance of logistics and operational coordination. Pandemic-related factory shutdowns and freight cost volatility demonstrated how sensitive margins can be to shipping disruptions. As a result, publishers increasingly favour larger, integrated partners capable of managing sourcing, production scheduling and freight consolidation across multiple regions. Vertically integrated models that combine print manufacturing, print management and publishing capabilities are therefore strategically advantageous.

Overall, the sector offers steady, recurring revenue streams rather than rapid expansion. Growth tends to come from market share gains, operational efficiency and disciplined acquisitions rather than underlying demand acceleration. In this environment, scale, cost control, geographic diversification and strong long-term relationships with international publishers are key competitive advantages.

Business Model

Lion Rock Group Limited operates a vertically integrated model that generates revenue across three main streams. Its core business is printing, producing books and illustrated publications for international publishers, educational institutions, and media companies. Revenue from this segment is recognised when products are delivered and accepted, and it benefits from the Group’s scale in procurement, efficient production processes, and geographically diversified facilities across Asia, Europe, and Australia.

The second revenue stream comes from print management and procurement services provided through subsidiaries such as Libermata and Asia Pacific Offset. These units act as intermediaries between publishers and printers, coordinating sourcing, supplier selection, production scheduling, logistics, and quality control. By consolidating orders and directing volumes to its own facilities, Lion Rock generates service fees while maintaining strong client relationships.

The third stream is publishing, primarily through its controlling stake in The Quarto Group. This business produces illustrated non-fiction titles and generates income from book sales, publishing rights, and royalties. Publishing provides strategic value by giving the Group insights into market trends and end-consumer preferences. Additional minor income comes from the sale of by-products such as recycled paper. By combining manufacturing, services, and content ownership, Lion Rock captures value across the full publishing supply chain while maintaining operational flexibility and scale advantages.

Shareholding Structure

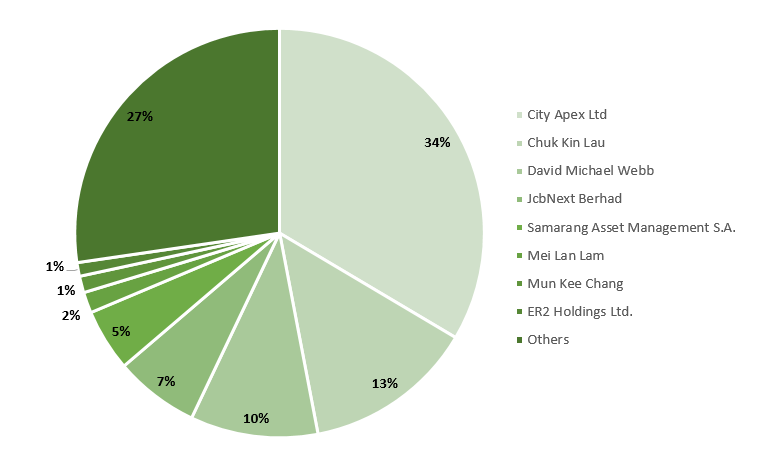

Lion Rock Group benefits from a shareholder structure that reflects strong alignment between management and investors. Founder and Chairman Lau Chuk Kin maintains a substantial personal stake, directly owning 13% of the company, demonstrating significant “skin in the game.” In addition, he serves as the principal shareholder and director of ER2 Holding Limited, which controls entities including City Apex Limited, Lion Rock Group, and Left Field Printing Group. Through City Apex, Lau indirectly controls an additional 35% of Lion Rock, resulting in a total effective ownership of 48% and ensuring strong alignment with long-term shareholder interests.

The shareholder register also includes reputable institutional and legacy investors. JCBNext Berhad, a Malaysia‑based investment holding company with stakes in digital and online marketing businesses and other quoted securities, owns roughly 7% of Lion, adding a reputable institutional holder to the register. The late David Webb, a highly respected advocate for transparency and shareholder rights, held a 10% stake, which is expected to pass to his family, likely maintaining the investment in line with his legacy. Former CFO Mei Lan Lam, who retired in August 2025 after joining the company in 2015, retains a 2% stake and was widely regarded for her steady and reliable stewardship during her tenure.

Risks

Trade volatility: Tariffs on Chinese-made books, particularly from US-China trade tensions, could increase costs or shift demand to alternative production sites.

Currency fluctuations: Movements in the Renminbi, Pound Sterling, Euro, and other currencies can impact costs, revenues, and margins across its global operations.

Digitalisation: The ongoing shift toward e-books and electronic media may reduce demand for physical printed materials over time.

Technological developments: Advances in printing technology, including digital presses and specialised inks, require adaptation to shorter print runs and faster fulfilment cycles.

Input cost volatility: Fluctuations in paper, ink, and energy prices can affect margins, as these costs are not always fully passed on to customers. In 2017, Lion Rock faced a 20% spike in paper costs, which led 1010 Printing to report a 10% revenue decline. Management avoided aggressive price competition, and some clients cancelled projects as rising input costs made certain titles uneconomical, highlighting the business’s sensitivity to commodity prices.

Logistics and supply chain disruptions: Freight delays, port congestion, and global shipping constraints can increase costs and affect delivery schedules.

Market consolidation: Mergers and acquisitions in the publishing industry can reduce the number of clients and shift bargaining power toward larger publishers.

Key Numbers

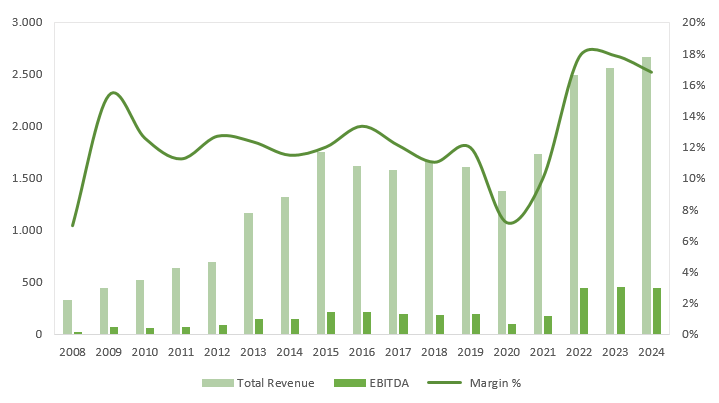

Lion Rock is a global book printing company led by a seasoned capital allocator, demonstrating consistent financial performance over the past 16 years. Revenue has grown at a CAGR of 14.6%, while EBITDA expanded at 21.3%, maintaining margins between 7% and 18%. Effective cost management has supported a net income CAGR of 19.7%, with an average net margin of 9%.

The company derives the majority of its revenue from the United States and Australia, exposing it to trade-related and geopolitical risks. U.S. tariffs on Chinese imports vary by product category: most general books are subject to a 7.5% Section 301 tariff, while calendars, planners, and certain other categories may face tariffs exceeding 30%. Exemptions apply for children’s picture books, board books, and religious materials. To mitigate exposure, Lion Rock has established production facilities in Malaysia (Papercraft) to serve U.S. demand, while operations in Australia (Left Field) and Singapore (COS) diversify the supply chain, manage labor cost pressures, and reduce reliance on China. Although paper costs in China remain 30–40% lower than in Western markets, providing a margin advantage, this gap could narrow if European energy and production costs decline.

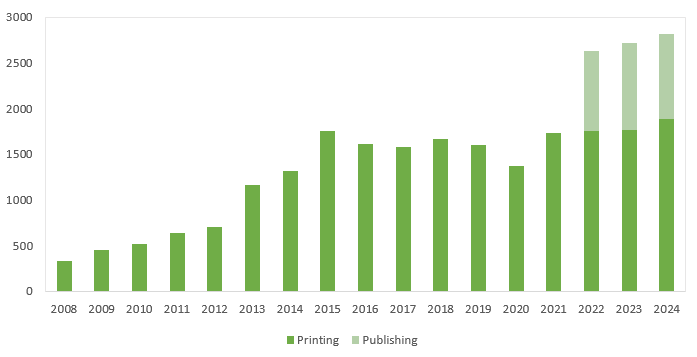

Lion Rock operates through two primary segments: Printing and Publishing. The Printing segment, which generates over 70% of total revenue, has achieved an 11.5% CAGR over 16 years. This segment benefits from a mature, efficient operational model, with automated processes, internalised workflows, and strategic capacity expansion that help control costs and support revenue growth. Management has characterised current conditions as favourable, driven by stable demand, incremental digital integration, and targeted expansion across Asia and Europe. The Publishing segment, which contributes the remainder of revenue, primarily involves distribution agreements and content licensing. Publishing is lower-margin due to higher development and marketing costs, a weaker market environment, and an ongoing reorganisation that temporarily compresses profitability. Despite lower margins, publishing provides strategic diversification, content ownership, and control over key intellectual property, complementing the more stable and profitable printing business.

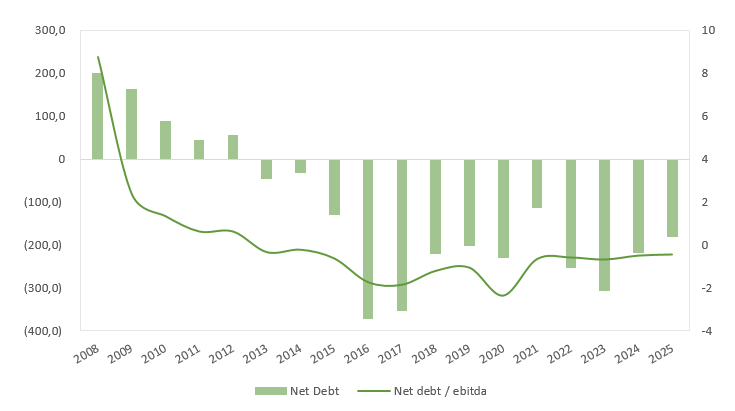

Financially, the company maintains a net cash position, with over HKD 180 million at the end of 2024, reflecting a net debt-to-EBITDA ratio of -0.4x. Holding this level of cash, while indicative of financial strength, may raise concerns among some investors due to minimal interest earned on large cash reserves and limited acquisition activity. Its asset-light operational model, with limited reliance on heavy machinery compared with traditional printers, supports operational flexibility, scalability, and strong liquidity. Capital expenditures are fully internally funded, reducing dependence on external financing. The company has recently refrained from acquisitions, as potential targets either exceed acceptable valuations or fail to meet short-term profitability thresholds. Debt associated with unrealised acquisitions has been gradually reduced, lowering financial costs and leverage from 17.2% to 14.5%, while preserving optionality through standby credit facilities. This disciplined approach emphasises balance sheet strength, net profitability, and financial resilience, positioning the company to pursue opportunistic, value-accretive investments.

Lion Rock remunerates shareholders mainly through regular interim and special dividends, which form the core of its payout policy. The company has maintained a consistent record of dividend payments even during challenging periods, with total dividends reaching HK$0.145 per share in 2024, paid through two interim and two special dividends. Dividend decisions are based on factors such as financial performance, liquidity, working capital requirements, debt obligations, and future expansion plans. In addition to cash dividends, the Group has occasionally returned value through alternative methods, such as the 2020 distribution in specie of shares in Left Field Printing Group Limited. Share repurchases are rare at the parent company level but may occur within subsidiaries for strategic purposes, for example the 2024 buyback by The Quarto Group linked to its voluntary delisting. As of December 2024, the Group held approximately HK$408 million in distributable reserves, indicating solid capacity to sustain future shareholder returns.

Valuation

Please note that the following valuation reflects the base-case scenario only, with downside risks modelled separately. Investors should conduct their own valuation analysis based on individual assumptions and projections. The valuation of Lion Rock is derived from a combination of methodologies, including a Discounted Cash Flow (DCF) model with a 6-year explicit forecast period and a relative valuation approach using EV/EBITDA and P/E multiples. This assessment forms part of a broader valuation framework incorporating additional scenarios and alternative methodologies to provide a more comprehensive estimate of intrinsic value. Accordingly, independent due diligence is recommended before drawing any investment conclusions.

The DCF model assumes the company can sustain an EBIT margin of 7%, reflecting a conservative assumption positioned at the lower end of the company’s historical range of profitability within a mature industry. A terminal growth rate of 0% is applied, consistent with the long-term outlook for the global printing sector, which is characterised by a flat to decreasing structural trend, albeit at a gradual pace. The weighted average cost of capital (WACC) of 14.3% incorporates the risk-free rate, equity risk premium, size premium, country-specific risk adjustments, and an additional stress premium reflecting current macroeconomic conditions. The discount rate also captures elevated geopolitical and trade risks, particularly potential U.S. tariff exposure, given that approximately 50% of Group revenue is generated in the United States. Based on these assumptions, the DCF analysis yields a fair value of HK$4.12 per share, implying upside potential in excess of 200% relative to the current market price.

Under the relative valuation framework, applying an EV/EBITDA multiple of 5.0x results in an implied equity value of HK$3.66 per share, while a P/E multiple of 10.0x implies a valuation of HK$3.83 per share.

Assigning equal weighting of 50% to the DCF and 50% to the multiples-based valuation produces a blended fair value of HK$3.93 per share. To account for potential optimism embedded in the underlying assumptions, a 10% margin of error is applied, resulting in a more conservative valuation. Even after this adjustment, the shares indicate an upside potential of approximately 164% relative to current trading levels.

Conclusion

Lion Rock Group, led by founder Chuk Kin Lau, is a vertically integrated book printing and publishing platform with a track record of disciplined growth, operational efficiency, and strategic acquisitions. Despite operating in a mature industry, the company benefits from scale, geographic diversification, vertical integration, and a focus on resilient illustrated and educational book segments. Key risks include potential U.S. tariff exposure, input cost volatility, currency fluctuations, and broader industry headwinds. Strong cash generation, a net cash position, and substantial founder ownership align management with long-term shareholder value. Current market valuation appears to understate the company’s intrinsic worth, suggesting meaningful upside potential as its strategic execution and operational strengths continue to be recognised.

Personal note: The company demonstrates strong management; however, current tariff-related tensions represent a significant risk. With rising energy costs driven by the conflict in the Middle East, the outlook remains uncertain. The company will continue to be monitored closely.

Disclaimer: All information provided herein by smallvalue is for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in any security. Smallvalue may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason.

Thanks to smallvalue. for highlighting Lion Rock Group Limited (1127; 1127 HK).

(a) Capitalisation of pre-publication costs started from 2022 and has become material. In 2024, addition to pre-publication costs amounted to ~64% of net profit. The amount net of amortisation is HKD 22 mn. This lifted 2024 net profit by ~11%.

Any idea why they started capitalisation of pre-publication costs in 2022? How appropriate is the capitalisation of these costs?

(b) Between 2015 and 2024, revenue increased 52% but inventory tripled. Days inventory has reached 92 days in the last twelve months. Any idea why?

Lion Rock’s low valuation is likely to reflect a structural jurisdictional discount such as diminishing political autonomy in Hong Kong, limited legal certainty and latent capital controls risks. In the extreme scenario of a conflict over Taiwan, capital tied up in Hong Kong would likely face severe disruption.

— 2025 update")

Thanks to smallvalue. for highlighting Lion Rock Group Limited (1127; 1127 HK).

(a) Capitalisation of pre-publication costs started from 2022 and has become material. In 2024, addition to pre-publication costs amounted to ~64% of net profit. The amount net of amortisation is HKD 22 mn. This lifted 2024 net profit by ~11%.

Any idea why they started capitalisation of pre-publication costs in 2022? How appropriate is the capitalisation of these costs?

(b) Between 2015 and 2024, revenue increased 52% but inventory tripled. Days inventory has reached 92 days in the last twelve months. Any idea why?

Lion Rock’s low valuation is likely to reflect a structural jurisdictional discount such as diminishing political autonomy in Hong Kong, limited legal certainty and latent capital controls risks. In the extreme scenario of a conflict over Taiwan, capital tied up in Hong Kong would likely face severe disruption.