I hope you are enjoying a pleasant summer. I am pleased to share the latest update on the portfolio with you. I trust you will find this update insightful.

The second quarter of 2025 did not unfold as I anticipated, largely due to the sharp depreciation of the US dollar. Nevertheless, I had foreseen volatility. Since the inception of smallvalue through June 30, 2025, the portfolio has generated a cumulative return of 113.37%, corresponding to an annualized return of 16.65%. During Q2 2025 alone, the portfolio increased by 10.06% in euros, significantly outperforming key benchmarks, with the S&P 500 rising 2.00%, the Nasdaq 8.6%, and the Global Small-Cap Index 2.24%.

This strong quarterly performance was driven primarily by Toya S.A., whose share price rose by over 24% during the period. In Q1 2025, the company reported an 18.5% year-over-year increase in revenue, reaching PLN 231.9 million, and a 51.3% increase in net profit, totaling PLN 24.6 million. Profitability also improved, with the net margin rising to 10.6% (from 8.3% in Q1 2024) and the gross margin reaching 33.4%. Toya maintains a solid financial position, with a Net Debt/EBITDA ratio of just 0.62x, reflecting prudent and efficient capital management. Geographically, the company achieved strong growth in Poland (+19.3%), Romania (+11.9%), Ukraine (+59.3%), and Asia (+76%), with more moderate gains across Europe, Africa, and Latin America. This contributed to a 22.6% increase in export revenues, which totalled PLN 82.8 million. Effective inventory management also supported cash flow, reinforcing the strength and resilience of its operating model.

Orsero also posted robust results, with its share price rising by over 16% during the quarter. I will provide further detail on this position later in the letter. Meanwhile, gold remained an important component of the portfolio’s performance. My investment thesis remains fully intact, and despite the narrowing spread between gold miners and physical gold, I continue to hold the position. Investor demand for gold remains strong, with net inflows into gold ETFs approaching $40 billion year-to-date, and projections suggesting this could reach $80 billion by year-end.

On the other hand, Olvi Oyj delivered a flat performance, while Sprouts Farmers Market and Sanlorenzo posted modest gains of approximately 3%. Sprouts, a USD-denominated position, continues to represent a significant allocation within the portfolio, as does Mama’s Creations—also in USD—which delivered a strong return of over 30% during the quarter. However, the depreciation of the US dollar—down 14% year-to-date—has weighed on euro-denominated returns for our USD holdings. As stated from the outset, we do not hedge currency exposure and continue to uphold this approach. Currency risk is an inherent part of our global investment strategy; while it can affect short-term performance, it is fully accounted for within the portfolio’s overall risk framework.

During the second quarter of 2025, US equity markets showed a moderate recovery following the volatility experienced earlier in the year, although political uncertainty continued to weigh on investor confidence. The Trump administration maintained an unpredictable stance on key issues such as NATO relations, tensions in Asia, and trade policy, which constrained risk appetite. Additionally, macroeconomic data increasingly signalled weakness, while inflation remained elevated, contributing to economic stagflation. In contrast, despite ongoing economic softness in the Eurozone, European markets continued to rally. Investors appear to be rotating toward European assets, attracted by the relatively lower valuations found here, particularly in small-cap stocks.

Looking ahead to the third quarter, the market is expected to remain volatile, influenced by geopolitical tensions, trade disputes, and general economic weakness. However, I’m not here to make predictions. My focus is solely on the portfolio companies and generating new ideas. I will seek to capitalize on market opportunities to expand my positions or add companies from my watchlist.

“Nobody can predict interest rates, the future direction of the economy or the stock market. Dismiss all such forecasts and concentrate on what’s actually happening to the companies in which you’ve invested.” Peter Lynch

Investment Mistake

While I value learning from the mistakes of others, I also believe it is essential—both as an exercise in transparency and for your benefit—to share my own missteps.

Another mistake occurred on February 9, 2021, when I invested in Nicolás Correa, a company founded in 1947 in Eibar (Gipuzkoa) that specialises in milling solutions. Nicolás Correa offers a diverse portfolio of machines, including fixed-bed, gantry, movable column, and T-configuration models, with thousands of units deployed worldwide across industries such as aerospace, automotive, railway, energy, oil & gas, defense, and capital goods. The company’s operations are supported by several strategic subsidiaries: GNC Calderería, focused on welded mechanical structures; GNC Hypatia, which manufactures smaller milling machines; GNC Electrónica, specialising in electrical panels; and GNC Kunming, which serves the Asian market with standardised equipment.

I purchased shares at €4.70 each. Despite the company’s continued strong performance under an experienced management team, I sold my position on June 21, 2023, realising a return of 22.34% (excluding dividends). The mistake, however, was selling too early due to impatience. Since then, the stock has appreciated by 82.60%, plus dividends, meaning this investment had the potential to generate significantly greater returns.

This experience has underscored the importance of patience when investing in less liquid, small- and micro-cap companies. When the underlying investment thesis remains intact, exiting a position prematurely is often a costly mistake. I remain committed to learning from these experiences and continuously refining my approach, fully aware that many more lessons—and undoubtedly more than a few mistakes—lie ahead as I continue this journey.

“Show me a person who has never failed, and I will show you a failure of a person. What we learn from failure, and what we do with that knowledge, is what matters – and it's what makes us who we are.” Michael Bloomberg

Portfolio overview: Investments and Divestments

During the second quarter, no divestments were made. However, I initiated a new position in Caltagirone SpA and increased my stake in Orsero SpA. Both companies demonstrate strong financial fundamentals and a clear alignment between management and shareholders, underscoring a solid commitment to long-term value creation. Below is a summary of these investments:

Caltagirone SpA: diversified Italian holding company—controlled by the Caltagirone family—active in cement, construction, real estate, media, and finance. Founded in 1892 and led since 1984 by Francesco Gaetano Caltagirone, the group has evolved into a global industrial conglomerate. Its core asset, Cementir Holding (the family holds a total indirect and direct stake of 72.26%, while the Caltagirone Group controls 47%), is the world leader in white cement, operating in 18 countries. Under its current leadership, the group has delivered consistent growth, with a 25-year revenue CAGR of 7.38% and an EBITDA CAGR of 6.28%, while maintaining a stable EBITDA margin of 16%.

Despite past challenges—including the 2008–2012 financial crisis, which revealed vulnerabilities in the construction and media sectors—the company has shown remarkable resilience through effective asset restructuring and strategic acquisitions. Today, it boasts a strong financial position, characterised by a net cash balance and robust free cash flow generation exceeding 50%, underscoring a prudent and conservative capital allocation strategy typical of family-controlled businesses.

Trading at a normalized P/E ratio of just 6.6x, Caltagirone appears significantly undervalued despite its strong operational performance and high-quality assets. The company’s core cement business—an industry leader—alone trades at a discount, underscoring the group’s overall valuation gap. With the family maintaining over 87% ownership, Caltagirone benefits from steadfast long-term strategic alignment. Its diversified portfolio includes more than 1,400 managed properties, six leading regional newspapers in Italy, and equity stakes in prominent financial institutions such as Assicurazioni Generali and Mediobanca, all of which contribute to the group’s resilience and diversification.

While risks remain—particularly regulatory exposure in the cement sector, succession issues in governance, and vulnerability to macroeconomic and commodity price fluctuations—the group’s model, centered on strategic control, diversification, and financial discipline, positions Caltagirone as a significantly undervalued investment with high medium- to long-term revaluation potential. Its adjusted intrinsic valuation suggests an attractive margin of safety, supported by asset quality, family stability, and a strong value creation track record.

Orsero SpA: We increased our position in Orsero SpA ahead of its earnings release, anticipating strong results. Year-to-date, the stock has appreciated by 10%, as the market gradually begins to recognise its intrinsic value. This is a company that demands patience, and no—I will not repeat the same mistake I made with Nicolás Correa. Orsero is well-managed, and I’ve had the opportunity to speak directly with its excellent management team.

Orsero commenced 2025 with strong operational and financial momentum, reporting first-quarter net sales of €379.6 million, up 12.3% year-over-year, primarily driven by a 12.6% increase in its Distribution division—fueled by higher volumes and a richer premium fruit mix—while the Shipping segment posted modest growth of 1.9%. Adjusted EBITDA rose 28% to €21.5 million, with margin expansion to 5.7%, and net income surged 50% to €7.5 million, reflecting enhanced product mix and improved operating leverage. Free cash flow was solid at €11.7 million, supported by an €11.1 million working capital release, while operating capex reached €3.1 million, targeting strategic initiatives such as the new Verona warehouse, ERP upgrades across Italy, Spain, and Portugal, expansion projects in Seville, and logistics enhancements in key European markets. The company closed the quarter with €85.7 million in cash and a net financial position of €59.9 million (€115.1 million including IFRS 16 liabilities), underscoring its disciplined and efficient financial stewardship. Management maintains a constructive outlook for the full year 2025.

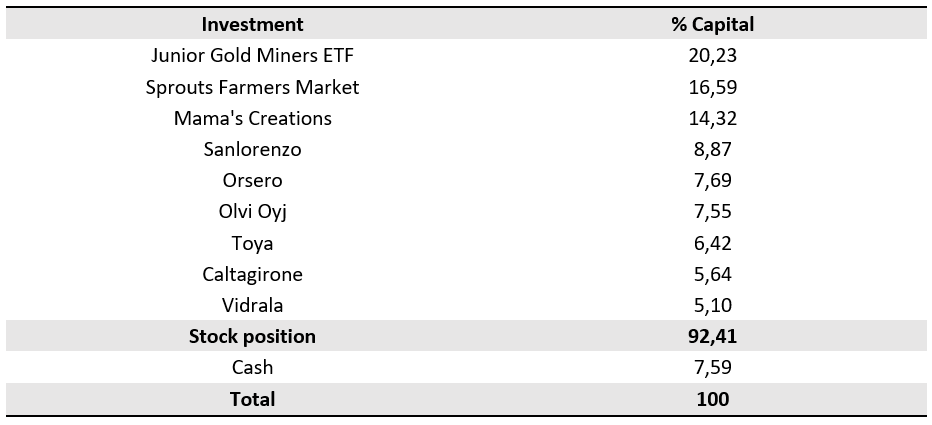

The following table provides a snapshot of the current investments in the portfolio:

Conclusion

I maintain strong conviction in our portfolio positions and continue to manage liquidity with a disciplined and prudent approach, fully aligned with our long-term investment philosophy. The companies I hold exhibit robust fundamental qualities and remain undervalued relative to their intrinsic worth, reinforcing our confidence in the portfolio. I believe it is only a matter of time before the market appropriately recognizes their true value. Regarding gold, the valuation gap is steadily closing in accordance with our thesis; despite the narrowing margin of safety, we will retain our gold ETF exposure until the discrepancy diminishes further. As always, I will exercise independent judgment in decision-making, capitalizing on opportunities where valuations are compelling and aligned with our goal of generating sustainable, long-term value.

Looking forward to the upcoming quarters — the second half of the year promises to be an exciting one.

Thank you for your continued support and trust in smallvalue.

Disclaimer: All information provided herein by smallvalue is for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in any security. Smallvalue may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason.

Congrats!

I see your second biggest position is Sprouts Market but I don't see a write up about it nor your history with it (ie when you entered the position etc) Thank you

I'm an economics student looking forward to working as a portfolio manager. I learned a lot about real company analysis and financial decision-making. Thank you, and I´ll wait for future updates.