Caltagirone SpA

Top-tier management team. Succession plan. Attractive valuation. Clear path to value creation.

Brief Summary: Caltagirone S.p.A. is a major Italian family-controlled holding company active in cement, construction, real estate, media, and minority stakes in finance. Founded in 1892 and led by Francesco Gaetano Caltagirone since 1984, its key asset Cementir is a global leader in white cement, operating in 18 countries. The group has a strong financial position, steady growth, and a diversified portfolio. Currently, it trades at a normalized P/E ratio of 6.3x, reflecting a significant discount despite solid fundamentals and long-term family control, making it an attractive investment with notable upside potential.

Company Overview

Founded in Rome in 1892 as a cement manufacturer, Caltagirone has grown into one of Italy’s leading conglomerates, with diversified operations across infrastructure, cement, real estate, media, and strategic investments, including minority stakes in financial institutions. The group’s transformation accelerated in 1984 when Francesco Gaetano Caltagirone took control, driving international expansion and sector diversification. Key milestones include the acquisition of Cementir in 1992, which established the group as a global leader in white cement through targeted international acquisitions, and the creation of Caltagirone Editore in the mid-1990s, marking its entry into the media sector with historic newspapers like Il Messaggero.

In recent years, the Caltagirone Group has focused on streamlining its portfolio and governance to enhance strategic agility, including the delisting of Vianini Lavori and restructuring under Domus Italia. Today, the group operates through a lean, integrated structure that balances its industrial heritage with forward-looking management. Listed on the Milan Stock Exchange, it combines professional leadership with family continuity, maintaining a long-term vision centred on innovation, value creation, sustainable growth, and strategic investments.

At the centre of this long-term vision is Francesco Gaetano Caltagirone, one of Italy’s most influential businessmen. Born in Rome in 1943, he has led the group’s transformation with a deep understanding of both market dynamics and institutional responsibility. In addition to his leadership within the group, he serves as Vice Chairman and is the third-largest shareholder of Assicurazioni Generali. He also holds significant equity positions in Suez Environnement, Acea, and Mediobanca—where he is one of the largest private shareholders, with a stake close to 10%. Over the course of his career, he has been honoured with the Order of Merit for Labour in recognition of his contributions to Italian industry.

The Caltagirone family plays an active role in the group’s operations. His children—Francesco, Alessandro, and Azzurra—hold senior executive roles across the business, ensuring a stable and well-prepared succession. Their involvement reflects the group’s long-standing commitment to continuity, innovation, and responsible growth. With a heritage built on resilience and a strategy geared toward the future, the Caltagirone Group continues to shape key sectors of the Italian and international economy.

Main companies of Caltagirone

Cementir Holding (47%): Controlled by the Caltagirone family, which holds a total direct and indirect stake of 72.26%. Cementir was acquired in 1992 by Francesco Gaetano Caltagirone through a competitive auction organised by the state-owned IRI group, marking one of Italy’s first major industrial privatisations. Subsequently, under the leadership of Francesco Caltagirone Jr. from 1996, the company underwent significant restructuring and global expansion. Today, it operates as a multinational group present in 18 countries with more than 70 sites. Cementir is a global leader in white cement production and exports, with an annual capacity of 3.3 million tons across six plants on four continents. The company also provides integrated building solutions including grey cement, lime, aggregates, concrete, and high-value-added products. Cementir holds key market positions as the sole cement producer in Denmark, ranks third in Belgium, is a major player in Turkey, and leads the concrete market in Scandinavia. It is listed on the Milan Stock Exchange and remains under majority control of the Caltagirone family.

Caltagirone Editore S.p.A. (60.764%). Founded in 1999 by Francesco Gaetano Caltagirone, Caltagirone Editore S.p.A. is one of Italy’s leading publishing groups and has been listed on the Milan Stock Exchange since 2000. The company owns and manages several of the country’s most prominent and widely read regional newspapers, including Il Messaggero (Rome), Il Mattino (Naples), Il Gazzettino (Venice), Corriere Adriatico (Marche), Nuovo Quotidiano di Puglia (Apulia), and the free daily Leggo. It also operates through subsidiaries such as Piemme S.p.A., which manages advertising, and CED Digital & Servizi S.r.l., which focuses on digital and technological solutions. Its organisational structure effectively integrates editorial, commercial, and digital operations, consolidating its leadership in Italy’s media landscape. With a strong national presence and loyal readership, the group is a major force in the Italian press. The Caltagirone family maintains a majority stake, ensuring strategic alignment with the group’s founding values.

Vianini S.p.A. Vianini Lavori, and Vianini Industria are two historic Italian companies that became part of the Caltagirone Group in 1984, when Francesco Gaetano Caltagirone acquired control of the Vianini group. Founded in the 1920s, Vianini Lavori specialises in major infrastructure projects both in Italy and abroad. It has been involved in landmark projects such as Rome’s Metro Line C, the Rome–Naples high-speed railway, and numerous dams, tunnels, aqueducts, and ports worldwide. In 2015, it was delisted from the Milan Stock Exchange to facilitate the group’s strategic reorganisation. Vianini Industria, originally established in 1980 and focused on reinforced concrete products, reoriented its strategy in 2016 following the acquisition of Domus Italia. It subsequently became Vianini S.p.A., shifting its focus to the real estate sector. Today, both companies continue to operate as key pillars within the Caltagirone Group, each playing a specialised role in infrastructure and property development.

Domus Italia S.p.A. Based in Rome, Domus Italia S.p.A. joined the Caltagirone Group in 2016 following its acquisition by Vianini Industria S.p.A., which later adopted the name Vianini S.p.A. to reflect its new focus on real estate. Domus Italia specialises in the management, leasing, sale, and maintenance of residential properties. It currently oversees around 1,400 housing units in Rome, offering comprehensive services to both owners and tenants. While operating under Vianini’s umbrella, Domus Italia maintains a distinct identity within the group, focusing on residential property management. This strategic focus strengthens the Caltagirone Group’s diversification efforts in complementary sectors.

Financial Entities' Stake: Assicurazioni Generali, with a 1.4% stake, is one of the leading European insurance groups, renowned for its financial strength and extensive experience in the insurance sector, providing stability and confidence to the company. Mediobanca, holding 1%, is a prominent Italian investment bank specialising in corporate banking and financial advisory, playing a key role in facilitating capital access and supporting strategic growth.

Note: The rest of the stake shown on Generali’s website (6.90%, which has recently increased) or the one listed on Mediobanca’s (7.391%, also recently increased) does not belong to Caltagirone S.p.A. These holdings are registered under Francesco's name and are therefore not counted when assessing the holding company’s total stake.

Business Model

Caltagirone S.p.A. operates as a diversified holding company with a business model focused on strategic ownership, governance, and financial oversight of a portfolio of leading companies across key sectors of the Italian and global economy. The group’s long-term strategy emphasises value creation through stable investments in strategic industries, supported by a strong industrial and institutional vision.

Shareholding Structure

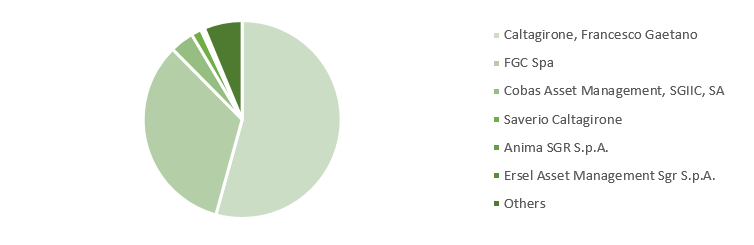

Francesco Gaetano Caltagirone is the principal shareholder of the holding, with a combined direct and indirect stake exceeding 50% of the group's share capital. Another major shareholder is FGC S.p.A.—the family investment vehicle controlled by Alessandro and Azzurra Caltagirone, his children—which holds a 33.3% stake. Together, the Caltagirone family exercises control over approximately 87.6% of the company, ensuring absolute majority ownership and long-term strategic continuity.

Additional family members, such as Saverio Caltagirone, also maintain significant holdings—he owns 1.665%—underscoring the family’s deep commitment and personal stake (“skin in the game”) in the group’s success.

Among institutional investors, Cobas Asset Management stands out prominently. Additionally, smaller funds such as the Palm Harbour Global Value Fund, managed by Peter Smith, have identified Caltagirone as a core holding, demonstrating strong confidence in the group’s fundamentals and long-term prospects. We can also find Cinvest Nogal Capital FI, managed by Rodrigo Cobos.

Risks

Credit: Managed through creditworthiness assessments of clients and internal exposure limits, with no significant concentration in any single customer.

Environmental: The cement industry is one of the largest CO₂ emitters, and it may be subject to regulatory risk.

Liquidity: Considered low, thanks to the group's own available financial resources and constant monitoring of cash flows.

FX: International exposure is partially hedged through currency hedging contracts to mitigate potential impacts.

Interest rate: Exposure to variable-rate debt is partially mitigated through Interest Rate Swap agreements.

Fair value risk of equity investments: Constant monitoring of market prices and active investment/divestment strategies are in place to optimize returns and diversify risk.

Fair value risk of real estate investments: Properties are periodically appraised by independent experts, with ongoing market monitoring—primarily in Italy and Turkey.

Commodity price: Managed through forward contracts, supplier diversification, and the use of derivative instruments to hedge price fluctuations.

Succession: While the founder’s children and other family members have been actively involved in the group for many years, there remains some uncertainty regarding future leadership in the absence of Francesco Gaetano Caltagirone. Nevertheless, as a well-established family-owned group with extensive experience, the family is considered well-prepared to ensure continued effective management.

Key Numbers

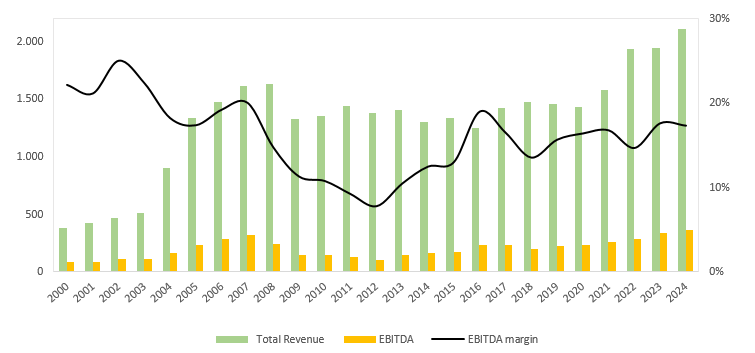

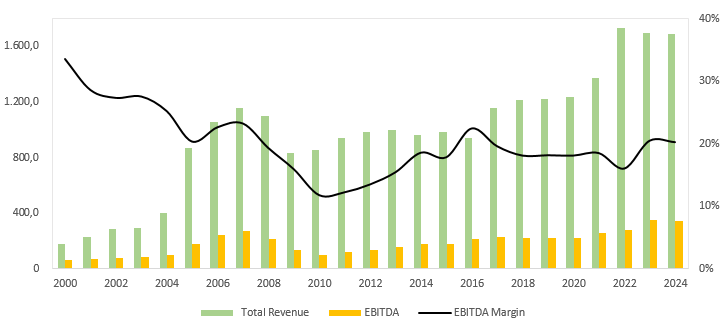

Caltagirone S.p.A. is the holding company of one of Italy’s most prominent business families, led by Francesco Gaetano Caltagirone, and has demonstrated a solid and consistent track record over recent decades. Over the past 25 years, the group has achieved a compound annual growth rate (CAGR) of 7.38% in revenues and 6.28% in EBITDA, maintaining a steady EBITDA margin of 16%. Operating income has grown at an annual rate of 9.51%.

During the global financial crisis of 2008–2012, the group experienced a significant margin contraction due to a sharp decline in demand in key sectors such as construction and cement. Additionally, a steep drop in advertising investment severely impacted the media division, while impairments related to investments in Banca Monte dei Paschi di Siena negatively affected results. These challenges were compounded by increased operating costs and expenses associated with restructuring processes (closures, layoffs), which substantially reduced the group’s profitability. Since then, Caltagirone has successfully recovered margins and clearly improved its operational efficiency.

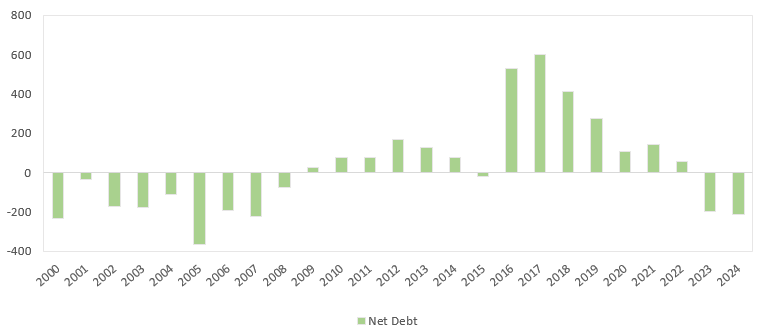

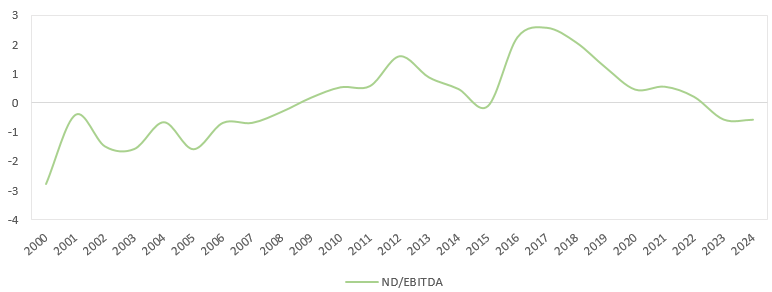

The group maintains a very solid financial structure, in line with Francesco Caltagirone’s conservative philosophy, which prioritises prudence in the use of family capital. The combination of low debt, consistent generation of operating cash flow, and a diversified investment portfolio provides financial stability and flexibility to pursue new investments.

Between 2016 and 2018, the group made significant acquisitions, including Cementir Sacci for €125 million, Betontir, and 100% of Domus Italia for €90 million, payable in two instalments. These companies, some of which were struggling after the economic crisis—such as Cementir Sacci, which had suffered demand declines and profitability issues—were acquired at attractive prices with the goal of revitalising them. Domus Italia, emerging from a challenging real estate market, was part of a strategy to consolidate and reorganise assets in sectors impacted by the downturn but with recovery potential. These transactions, partially financed with debt, reflect a strategy of expansion and consolidation in key sectors like construction and real estate, which explained the increase in the group’s indebtedness during that period. Currently, the group generates a high free cash flow, with a free cash flow yield exceeding 50%, further reinforcing its financial strength.

When discussing Caltagirone, it is essential to highlight Cementir S.p.A., its most significant asset. Cementir is a global leader in white cement production and holds strategic positions in countries such as Denmark, the United States, Egypt, Malaysia, China, and Australia. It is also the sole producer of grey cement and ready-mix concrete in Denmark, with a strong presence in Norway, Sweden, Belgium, and Turkey. Thanks to a growth strategy based on investments and acquisitions, Cementir has established itself as a multinational group operating in 18 countries, with a total capacity exceeding 13 million tons of white and grey cement. Annually, it sells approximately 10 million tons of aggregates and 5 million cubic meters of ready-mix concrete. In 2017, Cementir exited the highly competitive Italian market to focus on regions with higher margins and better growth prospects.

White cement, a specialized product significantly more expensive than grey cement, represents a global niche where Cementir holds nearly a 20% market share. Although it leads the market, its shares trade at a substantial discount compared to competitors. With zero debt and a strong market position, the company offers a cash flow yield close to 15%.

Over the past 24 years, Cementir has maintained a compound annual growth rate (CAGR) of 10.1% in revenues and 7.9% in EBITDA, with stable operating margins. Since 2022, the company has maintained a net cash position—meaning no financial debt—reflecting notable financial strength.

The cement market is projected to grow at a compound annual growth rate (CAGR) of 5-6% through 2028. However, in recent years, the sector has faced significant challenges due to rising energy costs and other raw materials. In this context, specialized companies like Cementir, known for their high operational efficiency, have managed to partially pass these cost increases onto selling prices.

During 2022 and 2023, sales volume measured in metric tons showed a slight contraction; however, prices followed an upward trend, allowing the company to maintain—and even improve—its profitability despite the inflationary environment.

We are looking at an industry with structurally solid prospects. Cement remains the most widely used synthetic material in history, thanks to irreplaceable structural qualities such as durability, availability, and low cost, which are essential for building construction and infrastructure. Although the macroeconomic environment remains uncertain, a recovery in the construction sector is expected, particularly in the residential segment, driven by supply shortages and structurally high demand, which will continue to benefit companies like Cementir. Additionally, despite the perception of the sector as one with undifferentiated products, Cementir holds significant competitive advantages. Entry barriers are high due to capital costs as well as regulatory and environmental restrictions that make opening new quarries difficult.

Overall, Cementir is an atypical case within a traditionally cyclical sector: a company that, thanks to its geographic diversification, leadership in the white cement niche, and proven financial discipline, projects a notably defensive profile.

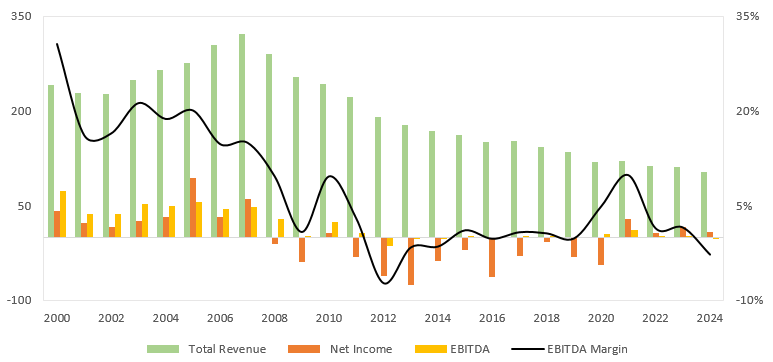

Caltagirone Editore, despite operating in a structurally declining sector—affected by sustained reductions in print newspaper circulation and the migration of advertising investment towards digital channels—maintains a relevant position within the Italian media landscape. The company publishes six of the country’s main newspapers, including Il Messaggero, Il Mattino, Il Gazzettino, Corriere Adriatico, Nuovo Quotidiano di Puglia, and the free daily Leggo.

In addition, it manages the advertising agency Piemme and the digital division CEDS Digital & Servizi, which specializes in technological solutions for both owned media and external clients. Through its various platforms, it reaches an audience of over 1.7 million daily readers and 3.9 million unique users, reflecting its relative weight within the sector.

Nevertheless, the group continues to face significant structural challenges. The ongoing erosion of traditional advertising revenue and growing competition from new digital media have put pressure on its business model. Although Caltagirone Editore has made efforts to adapt to the digital environment, the decline of the print media market considerably limits its long-term value creation capacity.

As shown in the accompanying chart, despite maintaining a competitive position “within what remains” of the sector, revenues continue their downward trend. From a valuation perspective, this division contributes a marginal weight within the overall Caltagirone group.

Domus and Vianini are expected to gain increasing importance within the holding and, in a few years, will represent a larger portion than Caltagirone Editore, given that the latter segment is in decline. The continued growth of Domus and Vianini is natural within the group, and we believe these divisions can add significant value to the holding.

Valuation

To keep this analysis concise, we will present a summary that values the holding company using a sum-of-the-parts approach and also apply a discounted cash flow (DCF) analysis to the entire group, considering a five-year time horizon.

It is important to note that this is a simplified summary based on more detailed work. That work includes additional models and separate valuations, such as a specific DCF for Cementir, among others. These approaches provide a broader and more robust understanding of the holding with different valuation scenarios. Readers are encouraged to conduct their own analysis, as this document represents only a high-level overview based on a base case.

1. Sum-of-the-parts valuation.

To simplify the analysis, this valuation primarily relies on relative multiples. While Cementir and Editore have also been valued using a DCF approach, those results are not included here, as this is only a summary of a broader analysis that considers multiple scenarios. Therefore, the valuation presented should be regarded as indicative rather than definitive.

Caltagirone Holding comprises several segments: the cement division, real estate and construction, the editorial business (Editore), as well as small equity stakes in Generali and Mediobanca.

For the cement division, I assume the company could trade at the sector median—slightly below its main peers—using a 7x EBITDA multiple. Cementir is the key player in this segment and benefits from the competitive advantages previously discussed. Currently, it trades at a discount of approximately 50–55%, implying that, through Caltagirone Holding, investors gain exposure to this business at a significantly reduced valuation.

In contrast, the editorial segment has minimal impact on the group's overall valuation. Given its ongoing decline and limited relevance, I have conservatively applied a 0x EBITDA multiple.

For Vianini and Domus, I apply 9x and 8x EBITDA multiples, respectively—slightly below the industry average to reflect a cautious stance and to account for the relatively overheated conditions in the real estate sector.

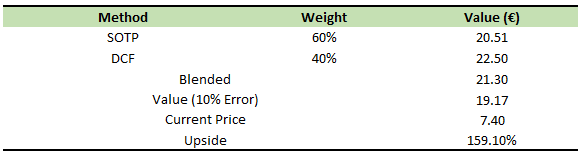

By applying these sector multiples to each business line, adjusting the aggregate enterprise value for net debt and minority interests, and incorporating a standard 20% holding discount—given that investment holdings typically trade at a discount—I arrive at an estimated equity value of €20.50 per share. This suggests an upside potential of over 180%.

2. Discounted cash flow (DCF)

The DCF analysis values the entire group with a time horizon extending through 2029. Key assumptions include an EBITDA margin of 18%, an EBIT margin of 12.3%, a terminal growth rate of 0.5%, and a weighted average cost of capital (WACC) of 12.90%. The terminal growth rate is conservatively set at 0.5%, as both the cement and real estate sectors are closely linked to GDP growth. In developed economies, long-term growth adjusted for inflation typically does not exceed 1% to 1.5%, and it is important to account for structural and regulatory risks.

The WACC includes an additional stress factor, representing a cautious adjustment to account for potential risks and macroeconomic volatility. This extra margin is designed to capture downside scenarios and ensure a conservative valuation. After discounting future cash flows using this stressed WACC, I apply an additional 20% discount to reflect the holding company structure, consistent with the typical market discount applied to such entities.

Based on these assumptions, the resulting valuation is €22.50 per share, implying an upside potential of over 200% compared to the current market price. This method is broadly consistent with my valuation based on the sum-of-the-parts approach.

Final valuation

By weighting the different valuation methods—giving greater importance to the sum-of-the-parts approach due to the ability to compare with similar competitors in each segment—I arrive at a target price of €21.30 per share. However, to mitigate optimistic bias and cover unforeseen events such as forecast errors or macroeconomic shocks, we apply a 10% margin of safety, resulting in an adjusted per-share value of €19.17.

Conclusion

Caltagirone is a diversified holding company with strategic exposure to sectors such as cement, construction, real estate, and minority financial stakes. Although it operates in a market with limited international visibility, the group benefits from clear competitive advantages and committed management, offering solid long-term growth potential. Its key assets, particularly Cementir, currently trade at a significant discount to their intrinsic value, presenting an attractive investment opportunity.

As a historic business with relatively low liquidity and the typical valuation discount applied to holding companies, the market may require more time to fully recognize its value. Despite challenges stemming from its conglomerate structure and market volatility, this situation provides a margin of safety for long-term investors. The shareholder structure and management’s commitment reinforce confidence in the holding’s ability to sustain value creation over time, making it an appealing option for those seeking a diversified investment with long-term appreciation potential.

Disclaimer: This is a personal analysis and does not constitute any buying or selling recommendations. Each investor should make their own due diligence.

Current forecasts likely underestimate geographic climate risk. If AMOC-driven disruption materializes, Caltagirone’s present revenue structure looks overexposed to Northern Europe, and its Italian growth prospects—while positive—would not be sufficient to fully offset a collapse in its top markets.

Hi there, good job on the write up. I have a question, we see from your analysis that CALT is mostly a bet on Cementir - the other holdings are not significant or could even lead to slight losses in bad years - every holding as a discount naturally applied. So my question is simple, why buy CALT instead of Cementir directly which remains quite cheap? thanks for your answer in advance