Happy New Year to everyone. I wish you all the best for 2026, and good health for all.

Before getting started, I would like to sincerely thank everyone for such an incredible 2025. Thank you to all who have read my posts, shared them, subscribed, or taken the time to provide feedback. Your support has been a tremendous motivation for me to continue growing and improving, both personally and as an investor. Once again, thank you very much.

This year has been a major learning experience and marks the second year in which I feel I have become a more independent thinker. In the early years, particularly when I started in 2020, I was heavily influenced by the opinions and commentary of others. Over time, my process has become far more disciplined and professional: I focus on thorough fundamental analysis, engaging in discussions with company management or investors close to the business when direct access isn’t possible, and conducting careful valuation. I no longer follow what is fashionable.

My portfolio, as many of you know, is composed of companies outside trendy sectors, with straightforward business models in traditional industries such as cement, food, and glass. While I may be sacrificing potential returns by not investing in high-profile names like Nvidia, Palantir, Broadcom or Tesla, I prefer confidence and stability in my holdings over chasing the next big winner. This approach allows me to focus on long-term value creation and reduces exposure to hype-driven volatility.

“Investing is not about beating others at their game…it’s about controlling yourself in your own game.” – Benjamin Graham

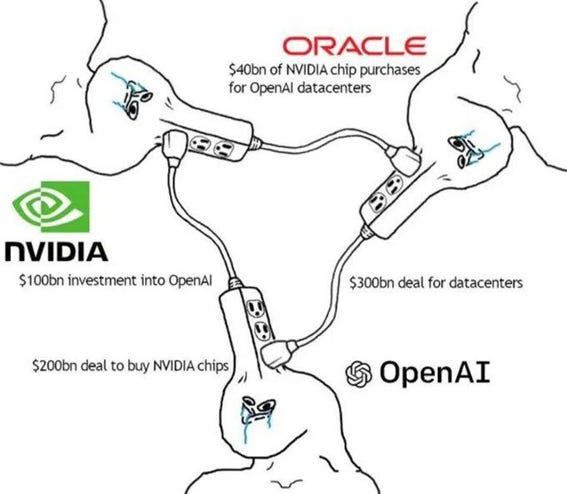

Artificial intelligence was undoubtedly the central theme of 2025, driving stock indices and sparking intense debate between those who believe “this time is different” and those warning of a bubble. The conversation is increasingly shaped by the massive capital required to build AI infrastructure, the enormous energy consumption, uncertainty over ultimate profitability, and the risk of asset depreciation. Personally, I wouldn’t dare say whether we are in a bubble or not—time will tell. I’m leaving a memo from Howard Marks for anyone who wants to read it, if you haven’t already.

Oracle provides a clear illustration. In Q2 of FY2026, its EPS beat expectations by 38%, but nearly all of that came from a one-time sale of Ampere Computing, while revenues fell short of projections. Its reported RPO stands at $500 billion, with $300 billion tied to OpenAI, but meeting those obligations requires a massive expansion of data centres—capex reached $12 billion versus the $8.4 billion expected, largely funded through new debt—while revenue growth and margins lag. A large portion of future revenue depends on a single customer, leaving the company exposed to concentration risk.

More broadly, AI-related capital investment is estimated to represent around 2% of U.S. GDP, highlighting the extraordinary scale, complexity, and risk inherent in this investment cycle.

Portfolio Performance

The fourth quarter of 2025 was positive, with a return of 6.55% for Q4. The year as a whole was marked by some market volatility, especially early on, driven by uncertainty around Trump’s tariffs and the back-and-forth signals from policymakers—announcing tariffs, delaying them, or retracting them—which created a climate of indecision that added further volatility. Overall, however, the portfolio had a strong year, delivering a return of 37.70% in euros, with relatively moderate volatility of 17.12% and a maximum drawdown of 12.50% in February, largely due to rising policy uncertainty and tariff concerns. For context, the S&P 500 in euros returned 4% over the year, while the MSCI World Small Caps returned 6%.

Since inception in 2020 through December 31, 2025, the portfolio has generated a cumulative return of 154.55%, equivalent to an annualised return of 18.82%. To be honest and realistic, I am still young and relatively inexperienced, and there is much for me to learn and improve upon. A significant portion of smallvalue’s performance is attributable to favourable market conditions and, to some extent, luck. While I take pride in having outperformed the broader market, true investment skill is proven over the long term. Six years is not enough to draw definitive conclusions, particularly without experiencing major market stress or a recession. As Warren Buffett wisely notes, “Only when the tide goes out do you discover who’s been swimming naked.” That is the test we are heading toward now, and it will be revealing to see where the portfolio stands during the next major market downturn.

Portfolio: What happened?

During the fourth quarter, I made no new investments or divestments. Sometimes, staying put can be the best decision; I’m not entirely sure if that was the case here, but it was the choice I made. I’d like to take a moment to share some thoughts on a few of the companies in my portfolio.

Who detracted from the portfolio? The biggest detractor for the portfolio was Sprouts Farmers Market, which declined 45% in 2025 (in EUR). While the company has continued to grow, it has done so at a slower pace, which led the market to react sharply, with a one-day correction of 27%. To be honest, the previous valuation of $170 per share was likely excessive, and part of the correction reflects that.

However, this remains a high-quality business. Sprouts has some of the best operating margins in its sector and continues to repurchase shares aggressively. Moreover, the company has ambitious expansion plans, aiming to triple its footprint from 450 to 1,400 stores nationwide. CEO Jack Sinclair has emphasised that the health-focused grocer plans to expand “from sea to shining sea,” while maintaining its fresh-first mission.

It is a steadily growing business with opportunities to open more stores and launch its own products, which should help better control costs and improve margins. The stock currently trades at approximately 15x earnings and 9x EBITDA, with a free cash flow yield of around 6%. The company benefits from expanding margins, a clean balance sheet, solid cash flow, and strong management—qualities that make it a compelling player in the grocery sector. The business still has strong long-term prospects, and we may see its stock return to around $150 per share.

Also on the negative side, Sanlorenzo declined nearly 7% in 2025. The company continues to grow and maintains a strong order book, but management projected growth at the lower end of its range and highlighted concerns about the U.S. market due to potential tariffs and policy uncertainty, raising questions about the sustainability of the Americas’ strong 39.9% YoY growth. The stock fell 7–8% in a single day, which I consider an overreaction by the market. I remain confident in the company’s execution and believe its value will be recognised over time. Holding Happy Life, the investment vehicle of Massimo Perotti, acquired a significant number of shares throughout the year, as I mentioned in previous letters, reflecting continued confidence in the business.

I would like to highlight a positive note for 2026, following a modest increase of just 7.4% in 2025. Olvi Oyj, a company I have summarised on my blog, deserves a brief recap here in case you are not familiar with it. The company is a Finnish small-cap with a €642M market capitalisation and continues to demonstrate strong fundamentals. Olvi benefits from substantial ownership, with over 16.19% held by the Olvi Foundation, and maintains solid financials. Valuation remains attractive, with low multiples of approximately 11x earnings and 8x EBITDA, suggesting potential undervaluation. Despite some illiquidity and geopolitical uncertainty in Belarus, Olvi’s long-term prospects remain promising.

In the latter part of 2025, Olvi announced a series of strategic acquisitions aimed at expanding its product portfolio and entering new markets, all scheduled for Q1 2026. These included Estonia’s leading mineral water producer, Värska Originaal, founded in 1993 with roots dating back to 1973 and offering natural, infused, and functional waters. Olvi has not yet specified the exact date of completion. In addition, Olvi acquired Banjalucka Pivara, Bosnia’s largest brewery, known for strong local brands such as Nektar lager and reporting €28M in revenue in 2024. The acquisition became effective on 2 January 2026, with ownership officially registered on 5 January 2026. These transactions are expected to expand Olvi’s non-alcoholic and alcoholic beverage portfolios, increase sales volumes, and strengthen production and export capabilities across the Baltics, Nordics, and Mediterranean markets. Finally, Olvi completed a 51% acquisition of Brewery International, a leading importer in Norway and Sweden, which employs 29 people and posted €22M in turnover in 2024. This transaction, finalised on 2 January 2026, immediately strengthens Olvi’s portfolio and market access in the Nordic region.

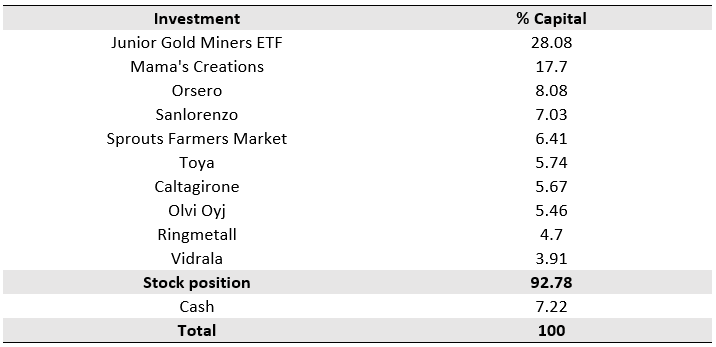

The following table provides a snapshot of the current investments in the portfolio:

What do I expect for 2026?

On the macro side, I honestly have no idea what will happen. The year has already started with some momentum, once again influenced by Trump, as was the case last year, driven by developments in Venezuela and his statements regarding other economies such as Mexico, Cuba, and Colombia. But we are not here to predict the direction of the economy. As Charlie Munger said, “We are not macro forecasters. Let’s focus on understanding businesses, not predicting recessions.”

That said, I would like to highlight a positive case for Europe. The continent faces a massive wave of capital investment: reindustrialisation, digitalisation, electrification, and defence/rearmament. Digitalisation, in particular, is highly capital-intensive: data centres are industrial facilities that require copper, steel, cement, concrete, and energy. Each megawatt of capacity requires tons of copper, cooling systems, and diesel backup generators. The cloud is not ethereal—it is heavy industry. The real beneficiaries, not immediately apparent, are not the data centres, real estate, or hyperscalers themselves, but the indirect players: industrial manufacturers, component distributors, and raw material suppliers. These are critical value-chain businesses with structural advantages and little competition.

An interesting case is copper. Without copper, there is no electrification, no digitalisation, no AI, and no data centres. Each megawatt of data centre capacity requires roughly 30 tons of copper; with 10,000 MW added annually, this amounts to approximately 300,000 tons—about 1% of the 30 million ton annual market. Even minor supply deficits in an already tight market can trigger significant price volatility, reinforcing a structural, long-term bullish outlook for copper.

That said, and paraphrasing Peter Lynch: “You cannot predict which sector will rise next year, but you can understand which companies will thrive, no matter what happens.”

What I do hope for in 2026 is that it will be a year in which I continue learning about investing, sharing companies, learning from investors much better than me, meeting interesting people, improving as a person, and above all, enjoying the process. Because don’t forget, that’s what it’s all about.

Conclusión

I remain firmly confident in the portfolio’s positions and continue to manage liquidity with discipline and prudence, fully aligned with my long-term investment philosophy. I acknowledge that mistakes are inevitable—and will continue to occur—as they are an inherent aspect of human decision-making. As we enter 2026 amid market uncertainty, I recognize that short-term market movements are inherently unpredictable. My focus remains on compounding capital at the highest rate achievable through a combination of skill, luck, and favorable market opportunities, making deliberate, well-informed decisions rooted in long-term prospects. In most cases, this approach requires patience.

I’m looking forward to an exciting year ahead, let’s enjoy it!

Thank you for your continued support and trust in smallvalue.

Disclaimer: All information provided herein by smallvalue is for informational purposes only and does not constitute investment advice or an offer or solicitation to buy or sell an interest in any security. Smallvalue may change its views about or its investment positions in any of the securities mentioned in this document at any time, for any reason or no reason.

Take a look about Next Geosolutions, i think its a very good value company. Btw very good year

Congrats! What drove the great performance? The Junior miners?